Research and Insights

Don’t call it a comeback – is inflation really returning and what does it mean for investors?

July 27, 2021

“Inflation is as violent as a mugger, as frightening as an armed robber and as deadly as a hit man.”

Those words by former President Ronald Reagan illustrate how dangerous inflation was considered to be when it reached its peak in recent American history, reaching 14.4% in early 1980. And they also explain why many investors with longer memories, including large institutional investors, are now concerned about the prospect of inflation returning.

Already this year the U.S. headline inflation rate has risen from 1.4% to 5.4% as of June, with rising commodities prices, a massive government stimulus program and supply-chain disruptions all seen as possible drivers of the increase. Investors are now considering if inflation is making a serious return, and if so, how they should position their portfolios for it.

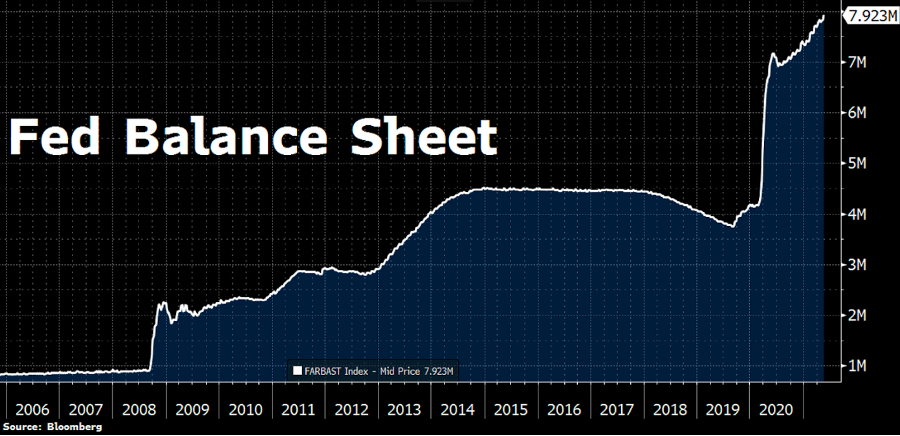

Of particular concern for many investors is the expansion of the Federal Reserve’s balance sheet. The Fed has doubled the size of its balance sheet since the beginning of the Covid-19 crisis, with it increasing from under $4 trillion to nearly $8 trillion (see graph below):

The Fed’s balance sheet could reach $9 trillion by the end of the year, according to a recent report by the NY Fed. According to conventional economic theory, this ought to have significant inflationary consequences. Milton Friedman famously said that, “Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.” This thesis is now being put to the test.

It is difficult not to see the current massive valuations of certain meme stocks and cryptocurrencies as indicative of market exuberance. And the combination of frothy markets and rising inflation has historically resulted in market corrections and rising interest rates. Economists Carmen Reinhart and Kenneth Rogoff argued in their 2009 book, “This Time It’s Different,” that experts and markets typically convince themselves that what has usually happened historically will not happen again because the current circumstances are somehow unique.

For a little historical perspective however, it is worth recalling that before the onset of the Covid-19 pandemic, deflation was more of a concern than inflation, which by 2019 had fallen to its lowest levels since 2016 in the U.S. and had dropped below 1% in Europe. On the supply side, a combination of globalization, technological developments, an energy and commodities supply glut driven by the shale boom, and slowing Chinese growth was driving input prices down. On the demand side, a combination of rising profit margins at the expense of wage increases and slower population growth was robbing the global middle-class of its purchasing power, dampening aggregate demand.

The Covid-19 pandemic changed all that. Shocks to global supply chains and record levels of economic stimulus from governments around the world, combined with the Biden administration’s focus on addressing social justice issues through major new spending initiatives, have culminated in an unprecedented situation of what is effectively wartime spending against the backdrop of a relatively healthy economy.

The main question for investors is whether higher levels of inflation which can be expected in the near term are transitory, or whether the world is right now on the brink of a new economic era. On the one hand, unprecedented expansion of the money supply and record low interest rates forecasts would indicate that increased levels of inflation are here to stay. On the other hand, the global economy has undergone transformative structural changes since the last period of high inflation in the 1970s. The deflationary pressures which have been suppressed for the last 18 months by government responses to Covid-19 are structural in nature and will not remain subdued indefinitely.

International commodities markets are now cheaper and more liquid than they were in the 1970s, and production of consumer goods is no longer concentrated in North America and Western Europe, where the supply of labor was limited and labor costs were high. New labor and consumer markets have become available globally as China and other emerging markets have opened up. This has resulted in consumer goods becoming cheaper in recent decades, exerting downwards pressure on consumer price inflation. In short, while powerful inflationary pressures have emerged, the capacity of the global economy to absorb them is arguably higher.

At Prelude, we believe that inflation will continue to rise in the short to medium term, but that eventually the deflationary factors that impacted the global economy before Covid-19 will re-emerge as a counterbalancing force. The result, we think, will be a booming global economy and a target-rich investment environment for hedge funds.

+++

Important Disclosure:

The opinions referenced above are those of the author as of July 27, 2021. These comments should not be construed as recommendations of any investment strategy or product for a particular investor, but as an illustration of broader themes. Forward-looking statements are not guarantees of future results. They involve risks, uncertainties and assumptions; there can be no assurance that actual results will not differ materially from expectations. Past performance does not guarantee future results.